Futures Market: Overnight, LME copper opened at $9,527.5/mt. Prices fluctuated at the beginning of the session, dipping to a low of $9,511.0/mt during the session, before fluctuating upward. Prices approached a high of $9,606.0/mt near the close and ultimately closed at $9,600.0/mt, up 0.08%. Trading volume reached 13,902 lots, and open interest stood at 293,706 lots. Overnight, the SHFE copper 2506 contract opened at 78,160 yuan/mt. Prices fluctuated at the beginning of the session, dipping to a low of 78,010 yuan/mt during the session, before gradually rising to a high of 78,610 yuan/mt. It ultimately closed at 78,490 yuan/mt, up 0.13%. Trading volume reached 27,647 lots, and open interest stood at 184,563 lots.

[SMM Copper Morning Meeting Summary] News: (1) The US dollar index fell amid slower retail sales growth in April and an unexpected decline in the month-on-month PPI. (2) Fed Chairman Powell: The Fed is adjusting its overall policy framework. Zero interest rates are no longer a baseline scenario. There is a need to reconsider the language on underemployment and average inflation. The April PCE is expected to fall to 2.2%.

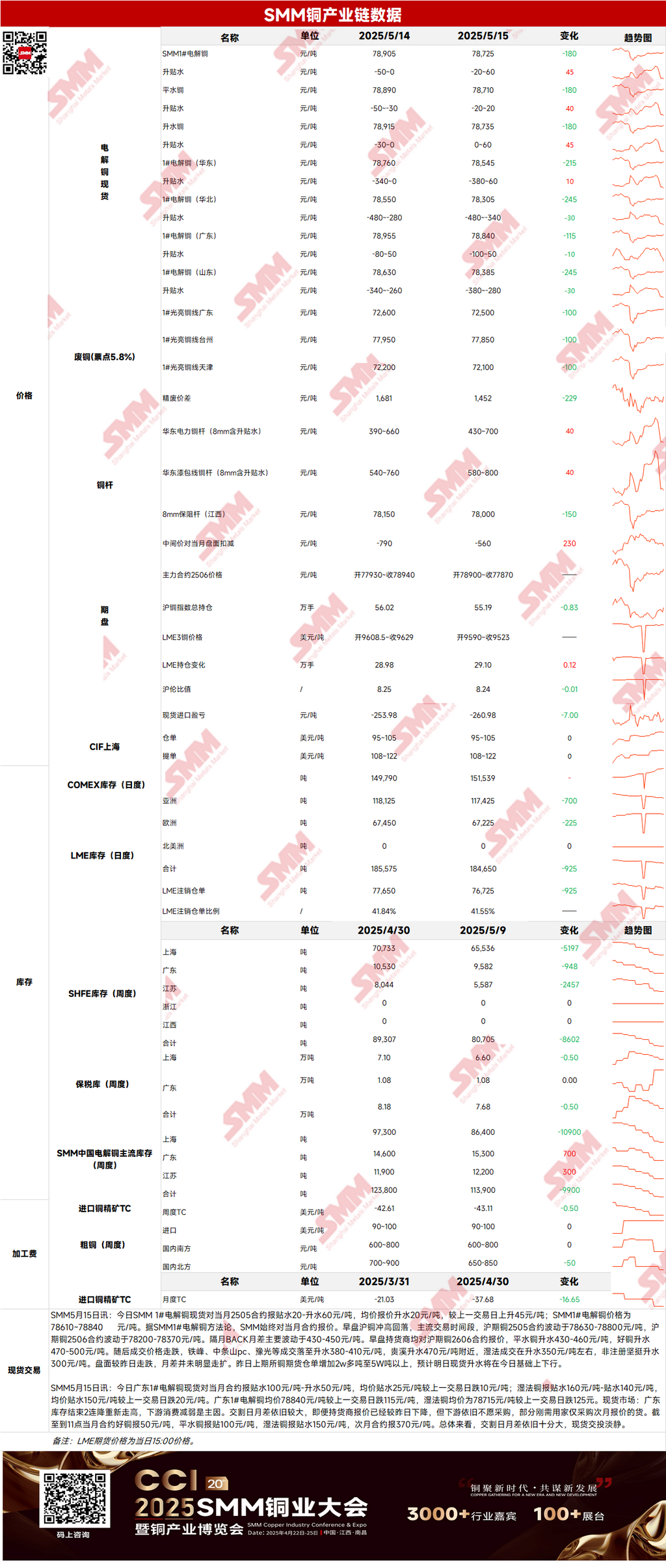

Spot: (1) Shanghai: On May 15, SMM #1 copper cathode spot prices against the front-month 2505 contract were quoted at a discount of 20-premium of 60 yuan/mt, with an average premium of 20 yuan/mt, up 45 yuan/mt from the previous trading day. The futures market declined compared to yesterday, and the price spread between futures contracts did not widen significantly. The previous day, SHFE copper futures warrants increased by over 20,000 mt to over 50,000 mt. It is expected that spot premiums will decline today compared to yesterday.

(2) Guangdong: On May 15, Guangdong #1 copper cathode spot prices against the front-month contract were quoted at a discount of 100 yuan/mt-premium of 50 yuan/mt, with an average discount of 25 yuan/mt, down 10 yuan/mt from the previous trading day. Overall, the price spread between futures contracts remained large during the delivery month, and spot trades were sluggish.

(3) Imported copper: On May 15, warrant prices were at $95-105/mt, QP June, with the average price unchanged from the previous trading day. B/L prices were at $108-122/mt, QP June, with the average price unchanged from the previous trading day. ER copper (CIF B/L) prices were at $76-88/mt, QP June, with the average price unchanged from the previous trading day. Quotations referenced cargoes arriving in mid-to-late May. The market performance was similar to that of the previous day, with the center of quoted prices for registered copper continuing to decline. The overall trading atmosphere was not active, and buyer counteroffers were low. It was heard that among traders, offers for domestic pyrometallurgy B/Ls for late May were at $110, QP June; general pyrometallurgy offers were around $115-120, QP June; domestic warrant offers were around $100-105, QP June; and offers for EQ B/Ls arriving in early June were at $90-95, QP June. Overall, the market was sluggish in the short term.

(4) Secondary copper: On May 15, the price of secondary copper raw materials fell by 100 yuan/mt MoM. Guangdong bare bright copper prices were at 72,400-72,600 yuan/mt, down 100 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,452 yuan/mt, down 229 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,125 yuan/mt. According to the SMM survey, sales of secondary copper rod continued to incur losses, prompting many enterprises to opt for production cuts. Those still in operation reported that nearly all daily output was being shipped out, suggesting a potential reduction in the market supply of secondary copper rod in the short term.

(5) Inventory: On May 15, LME copper cathode inventory decreased by 925 mt to 184,650 mt; on the same day, SHFE warrant inventory increased by 10,466 mt to 60,535 mt.

Price: On the macro front, the slower growth in US retail sales in April and the unexpected decline in the monthly PPI rate, coupled with a weaker US dollar index, pushed copper prices higher. Meanwhile, Putin's absence from the Turkey talks and the postponement of the Russia-Ukraine talks to the 16th also influenced the market. Domestically, Premier Li Qiang emphasized the importance of strengthening the domestic economic cycle as a strategic move to ensure steady and sustained economic growth. On the fundamental front, transactions for standard-quality copper against the SHFE copper 2506 contract moved downwards after a higher opening yesterday, closing at a spot premium of 380-410 yuan/mt. SHFE copper futures warrants increased by over 20,000 mt to more than 50,000 mt. As of Thursday, May 15, SMM's copper inventory in major Chinese regions increased by 8,900 mt from Monday to 132,000 mt, and by 11,900 mt from the previous Thursday, ending a 10-week consecutive destocking trend. The significant price spread between futures contracts led to a decline in downstream purchasing interest, with suppliers actively transferring inventory to delivery warehouses being the main reason. It is expected that spot premiums will continue to decline today compared to yesterday. Overall, with the US dollar index weakening again and today being the contract rollover day, copper prices are expected to find some support at the bottom and remain at highs.

》Click to view SMM Metal Database

[The above information is based on market collection and comprehensive assessment by the SMM research team. The information provided is for reference only. This article does not constitute direct investment research or decision-making advice. Clients should make cautious decisions and not rely solely on this information, replacing their independent judgment. Any decisions made by clients are unrelated to SMM.]